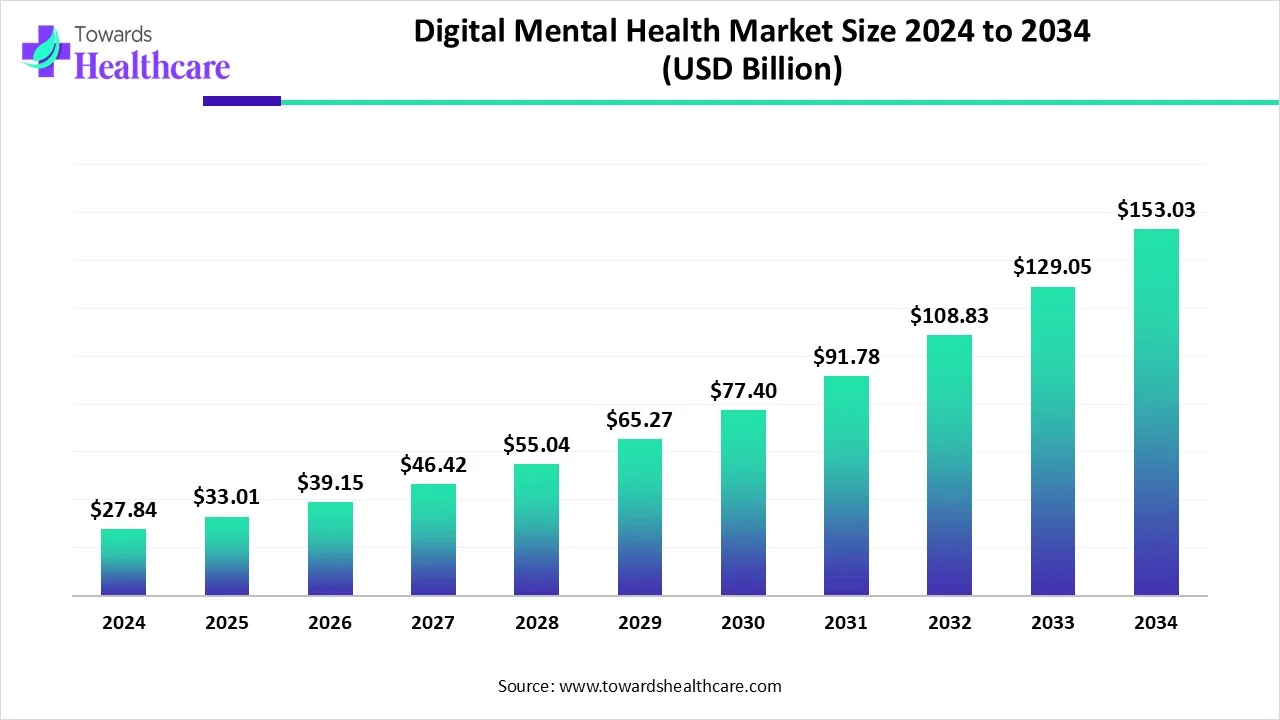

Digital Mental Health Market Size to Drive USD 153.03 Bn by 2034

The global digital mental health market size is calculated at USD 33.01 billion in 2025 and is expected to reach around USD 153.03 billion by 2034, growing at a CAGR of 18.58% for the forecasted period.

Ottawa, Oct. 14, 2025 (GLOBE NEWSWIRE) -- The global digital mental health market size was valued at USD 27.84 billion in 2024 and is predicted to hit around USD 153.03 billion by 2034, rising at a 18.58% CAGR, a study published by Towards Healthcare a sister firm of Precedence Research.

This market is rising due to rising prevalence of mental health disorders, increased awareness and acceptance, coupled with technology advances and a shortage of traditional mental health services are driving explosive demand for digital mental health solutions.

The Complete Study is Now Available for Immediate Access | Download the Sample Pages of this Report @ https://www.towardshealthcare.com/download-sample/5741

Key Takeaways:

- North America dominated the global digital mental health market in 2024.

- Asia Pacific is expected to be the fastest-growing during the forecast period.

- By component type, the software segment dominated the market in 2024 and is expected to be the fastest growing during the forecast period.

- By disorder type, the mental disorder segment dominated the market in 2024.

- By disorder type, the behavioral disorder segment is expected to be the fastest growing during the forecast period.

- By age group type, the adult (20 to 65) segment dominated the market in 2024.

- By age group type, the geriatric (above 65) segment is expected to be the fastest growing during the forecast period.

- By end user, the providers segment dominated the global digital mental health market in 2024.

- By end user, the patients segment is expected to be the fastest growing during the forecast period.

Market Overview:

The global digital mental health market is quickly expanding in response to the demand for remote care, the long-term pivot to teletherapy, and growing investment in digital therapeutics and mental wellness applications. While in-office therapy has struggled for decades with issues of access, affordability, stigma, and workforce shortages, digital health platforms are overcoming many of these barriers.

- In 2024, the market saw software solutions dominate the offering, as consumer preference began to favour platforms offering self-help tools, symptom checkers, chatbots, and virtual therapy.

Looking towards the future, anticipated growth from integration of artificial intelligence, wearables, personalized care and growing regulatory clarity is likely to support growth in the market. The projected growth is expected to be accelerated double digit CAGR through the late 2020s, also informed by growing consumer demand and the technological capability to respond to such demand.

Key Metrics and Overview

| Metric | Details | |

| Market Size in 2025 | USD 33.01 Billion | |

| Projected Market Size in 2034 | USD 153.03 Billion | |

| CAGR (2025 - 2034) | 18.58 | % |

| Leading Region | North America | |

| Market Segmentation | By Component, By Disorder Type, By Age Group, By End User, By Region | |

| Top Key Players | Talkspace, Woebot Health, Sonde Health, Inc., BetterHelp, CareTech Holdings PLC, Ieso Digital Health, Kintsugi Mindful Wellness, Inc. | |

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Major Growth Drivers:

- An uptick in the recognition and prevalence of mental health disorders: Mental health disorders including depression, anxiety, behavioral disorders and stress are being diagnosed more frequently than before, while the public education and awareness that has spread would lead consumers to seek help more than before. This is increasing the demand for solutions that can be scaled and delivered in a manner that is accessible to consumers.

- Technology proliferation (smartphones, internet, wearables) and AI/ML advances: The increase of the penetration of smartphones/internet worldwide along with advances in artificial intelligence, machine learning, and data analytics are enabling more individualized and real-time mental health monitoring or intervention.

- Telehealth/adoption of remote care: COVID-19 significantly sped up the uptake of remote mental health care for millions of patients when in-person care was disrupted. Now that things are returning to “normal,” both consumers and providers appreciate the convenience and flexibility of virtual/remote care.

- Supportive policy and funding environment: Governments, insurers and private investors are directing more and more funding to digital mental health platforms; reimbursement policies are being developed; even though regulatory clarity is slow, it is improving. This decreases risk and encourages more providers to enter the sector.

Become a valued research partner with us - https://www.towardshealthcare.com/schedule-meeting

Key Drifts in Digital Mental Health Market:

- More frequent use of AI chatbots and predictive analytics to provide just-in-time mental health interventions and track emotional well-being.

- Increased involvement of digital mental health platforms and traditional healthcare environments: EMRs, primary care, insurance companies are collaborating for holistic care.

- Priority is given to culturally sensitive, multilingual and localized content in apps and platforms for diverse populations.

- Increased attention on tracking and improving user engagement and adherence to plans, as most digital mental health interventions get strong early adoption but have high drop-off.

Major Limitations in Digital Mental Health Market:

One of the greatest challenges in the area of digital mental health is finding the appropriate balance between innovating and scaling new technologies while also prioritizing safety, effectiveness, and trust. Concerns about data privacy and security are at the forefront of this challenge because health-related data is often very sensitive and can cause harm if compromised or handled improperly.

Adding to these challenges, clinical validity is often lacking: many digital resources do not have strong randomized controlled trials or measures of efficacy and without some bench mark that clinicians and payers use to gauge safety and efficacy, will not feel confident using or recommending digital mental health resources.

Adding to the confusion are regulatory uncertainties; in many countries or sectors there is uncertainty if a digital mental health platform is a wellness app, medical device (Regulatory), or somwhere in between; reimbursement is complicated, and there is uncertainty regarding licensing and licensure across often borders. These are just a few of the barriers that can stymie adoption or increased cost of services or create distrust among users or health professionals.

Get the latest insights on life science industry segmentation with our Annual Membership: https://www.towardshealthcare.com/get-an-annual-membership

Regional Analysis:

What Made North America the Largest Shareholder in Digital Mental Health Market?

North America has been the largest market for digital mental health, due in large part to high healthcare spending, solid technological infrastructure, and a pre-existing telehealth market. The U.S. has witnessed increasing investment in the sector, increases in the adoption of digital therapeutics, and the inclusion of teletherapy in insurance reimbursement schedules.

In addition, regions with a high percentage of smartphone use, good internet access and increasing public and private awareness of mental health needs politically prop up electronic mental health interfaces. Notably, North American tech companies and startups are heavy investors in important technological initiatives in the region, focused on artificial intelligence, platform development and clinical validation, thus enhancing North America's place in relation to the rest of the world.

Asia Pacific Digital Mental Health Market Trends:

The Asia-Pacific region is the fastest-growing market segment, propelled by quick internet uptake, mobile adoption, and increased awareness of mental health, as well as burgeoning government initiatives. Countries like India, China, Japan, Australia, as well as Southeast Asian nations, are seeing demand and supply growth; more local apps, telehealth services, and digital wellness platforms are presented in local markets, even amongst significant challenges.

Despite challenges, forecasts for growth will continue to be strong, especially since companies are beginning to tap some very large, unserved populations. Countries in the region are viewing many digital mental health interfaces as needed, government sanctioned, solutions, as citizens are typically cost-sensitive, and require practical, scalable and low-cost options to their needs.

Download the single region market report @ https://www.towardshealthcare.com/checkout/5741

Segmental Insights:

By Component Type:

The software component of the digital mental health market commanded the greatest share given the increased adoption of mental health apps, symptom tracking tools, chatbots, virtual therapies, digital therapeutics, and remote monitoring software. As an egregrious example among end users, many paid for software-only or software-led solutions because they offered scalability, lower cost, ease of use, accessibility, and continual availability. A larger share of usage and interest in these software solutions helps facilitate ecosystems to develop that might enable more robust support and professional integration.

The software component should continue to grow the fastest during the forecasted period. Included in the rationale to allow for continued growth are the increasing demand for AI-based personalized features, convenience of software modules associated with wearable devices and medical record integration, and associated oversaturation of tech companies making investments in software development.

Lastly, as regulatory avenues provide clearer pathways and reimbursement improves, more resilient software-based digital mental health resources will be more feasible for providers and insurers. All these aspects of software combined support assurances that it will always remain in the same market leadership share, and same level of growth.

By Disorder Classification:

The segment related to mental disorders led the market, it is largely attributed to the high rates of mental disorders that exist and public attention toward mental disorders. The evidence-based mental health tools already available within the digital mental health space have largely focused on mental disorders, whether through digital applications that include cognitive behavioral therapy (CBT) modules or teletherapy resources.

Over the forecast period the behavior disorder segment is projected to grow the fastest. This development is as a result of heightened awareness of these conditions, improved diagnostic instruments and assessment measures, and an increased number of digital behavioral intervention programs being developed and more widely implemented.

By Age Group Type:

Individuals aged 20-65 represent the largest group currently using digital mental health services. Many within this age group are dealing with work-related stressors, transitional experiences in their lives, family obligations, and prefer technology therefore they are often first to adopt digital mental health solutions.

However, the geriatric (65+) population is anticipated to be the most rapidly growing population over the coming years. This trend is likely due to the aging population, increased awareness of mental health issues among seniors (e.g., depression, isolation, cognitive decline), increasingly usable interfaces and technological literacy for older users, and forms of remote monitoring and telehealth services that are particularly advantageous for older adults who may have limitations in mobility/transit.

By End-User:

The providers segment (hospitals, clinics, health systems, therapists utilizing digital platforms) constituted the largest market share in the digital mental health market. Providers use software, tele-therapy platforms, and digital therapeutics tools to facilitate service expansion, reduce cost, enhance patient outcomes, and manage the increase in patient volume. Providers typically contract with the platforms, work in workflows, and become the organization’s delivery mechanism of digital mental health care.

During the forecast period, patients (end-users) will have the fastest growth. More people are downloading the apps themselves, and using the digital therapy tool without involving a provider; self-help/ wellness apps, peer support tools, chatbot (AI) on apps, and direct-to-consumer digital therapeutics are growing in awareness. Further digital literacy and acceptance of digital tools, convenience preferences, and the reduction of stigma have favored patient-led options for mental health support.

Browse More Insights of Towards Healthcare:

The global supplemental health market is on a steady upward trajectory, expected to generate substantial revenue growth and potentially reach into the hundreds of millions between 2025 and 2034.

In the United States the supplemental health market was valued at US$ 38.62 billion in 2024, projected to rise to US$ 40.77 billion in 2025, and further expand to approximately US$ 65.19 billion by 2034, reflecting a CAGR of 5.64% during the forecast period.

Similarly, the global digital mental health platforms market is gaining strong momentum, rising from US$ 0.80 billion in 2024 to US$ 0.89 billion in 2025, and anticipated to reach US$ 2.49 billion by 2034, advancing at a CAGR of 12.37%.

The behavioral mental health market is also witnessing remarkable progress worldwide, with revenue expected to surge into the hundreds of millions between 2025 and 2034.

Meanwhile, the global AI in mental health market continues to accelerate, expanding from US$ 1.45 billion in 2024 to US$ 1.8 billion in 2025, and forecasted to reach around US$ 11.84 billion by 2034, growing at a robust CAGR of 24.15%.

The maternal mental health market is demonstrating exponential growth, increasing from US$ 10.32 billion in 2024 to US$ 13.25 billion in 2025, and projected to soar to US$ 126.33 billion by 2034, marking an impressive CAGR of 28.47%.

Additionally, the computational biology market is on a strong growth path, expected to rise from US$ 7.18 billion in 2025 to US$ 21.9 billion by 2034, registering a CAGR of 13.20% over the forecast period.

Furthermore, the chatbots for mental health and therapy market is projected to expand from US$ 1.77 billion in 2025 to US$ 10.16 billion by 2034, growing at a notable CAGR of 21.3%.

Lastly, the antipsychotic drugs market is anticipated to grow from US$ 20.96 billion in 2025 to US$ 41.21 billion by 2034, progressing at a CAGR of 7.8% over the same period.

Recent Developments:

In May 2025, the FDA announced that all its internal centers would begin deploying artificial intelligence tools immediately, aiming for full integration by June 30, 2025, following a generative-AI pilot for scientific review tasks.

Which are the Top 20 Companies in the Drug Discovery as a Service Market?

- Charles River Laboratories

- WuXi AppTec

- Evotec AG

- Covance (Labcorp)

- IQVIA

- Syneos Health

- Pharmaron

- PPD (Thermo Fisher Scientific)

- Medpace

- PRA Health Sciences

- BioDuro

- Frontage Laboratories

- ChemPartner

- KBI Biopharma

- Crown Bioscience

- Jubilant Biosys

- Recursion Pharmaceuticals

- Aragen Life Sciences

- Oncodesign

- TCG Lifesciences

Download the Competitive Landscape market report @ https://www.towardshealthcare.com/checkout/5741

Segments Covered in the Report

By Service Type

- Target Identification & Validation

- Genomic Target Discovery

- Proteomic Target Discovery

- CRISPR-based Validation

- Biomarker Discovery

- High Throughput Screening (HTS)

- Assay Development

- Compound Screening

- Phenotypic Screening

- Hit Identification & Lead Generation

- Fragment-Based Screening

- Virtual Screening

- Biochemical Screening

- Lead Optimization

- Medicinal Chemistry Support

- Structure-Activity Relationship (SAR) Analysis

- ADMET Optimization (Absorption, Distribution, Metabolism, Excretion, Toxicity)

- Preclinical Testing & Toxicology

- In vitro Toxicity Testing

- In vivo Animal Studies

- Safety Pharmacology

- Computational Drug Discovery

- Molecular Docking

- Molecular Dynamics Simulation

- QSAR Modeling

- AI & Machine Learning-based Drug Design

- Bioinformatics & Genomics Services

- Sequence Analysis

- Omics Data Integration

- Pathway Analysis

- Clinical Trial Support

- Biomarker Identification

- Patient Stratification

- Regulatory Consulting

- Consulting & Regulatory Support

- Regulatory Compliance Assistance

- Drug Development Strategy

- Intellectual Property (IP) Support

By Technology

- AI and Machine Learning

- Predictive Analytics

- De Novo Drug Design

- Biomarker Discovery

- High Throughput Screening

- Automated Screening Platforms

- Robotics Integration

- Molecular Modeling and Simulation

- Docking and Scoring

- Dynamics Simulations

- Genomics and Proteomics Platforms

- Next-Generation Sequencing (NGS)

- Mass Spectrometry

- Lab Automation & Robotics

- Sample Preparation Automation

- Data Capture Automation

- Data Analytics and Cloud Computing

- Big Data Analytics

- Cloud-Based Collaborative Platforms

By End User

- Pharmaceutical Companies

- Large Pharma

- Mid-sized Pharma

- Biotechnology Companies

- Contract Research Organizations (CROs)

- Academic and Research Institutes

By Therapeutic Area

- Oncology

- Cardiovascular Diseases

- Neurological Disorders

- Infectious Diseases

- Metabolic Disorders

- Autoimmune Diseases

- Rare Diseases

By Region

- North America

- U.S.

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/checkout/5741

Access our exclusive, data-rich dashboard dedicated to the healthcare market - built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

About Us

Towards Healthcare is a leading global provider of technological solutions, clinical research services, and advanced analytics, with a strong emphasis on life science research. Dedicated to advancing innovation in the life sciences sector, we build strategic partnerships that generate actionable insights and transformative breakthroughs. As a global strategy consulting firm, we empower life science leaders to gain a competitive edge, drive research excellence, and accelerate sustainable growth.

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Europe Region: +44 778 256 0738

North America Region: +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Automotive | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Towards Dental | Towards EV Solutions | Nova One Advisor | Healthcare Webwire | Packaging Webwire | Automotive Webwire

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest

![]()

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.